Role of Fintech in Shaping the Future of Banking in Nepal

Fintech, which is an abbreviation for economic technology, has been outpacing traditional banking in most countries around the world including Nepal. With the accelerating invasion of technology into financial services fintech is no longer just a new buzzword, but rather a path towards modernization of an old banking system. Fintech is clearly playing a key role in changing how banking services serve customers, developing financial inclusivity, and achieving a banking system that is more transparent, efficient, and customer experience driven, at the same time as the Nepali economy is maturing and the financial system is expanding.

Fintech Development in Nepal

In the last few years, there's been an observable impetus in fintech acceptance in Nepal, with the proliferation of the internet, increased access to smartphone ownership, and demand for improving financial service distribution due to increased competition. As articulated in the Nepal Bankers' Association article, the innovative solutions associated with fintech interventions have arguably been beneficial in regards to promoting financial inclusivity, a foundation of economic investment, and job creation. And while these solutions would not have existed a few years ago — as rural populations likely had limited access to technology-based financial solutions — today these technology solutions are reducing the financial technology gap between the unbanked and formal offerings.

The government has offered leadership towards initiating a fintech revolution around the country through the government's Digital Nepal Framework and its initiatives for cashless payments. Movements initiated by the National Bank of Nepal, Nepal Rastra Bank (NRB) have been essential moving forward in the growth of fintech in Nepal, with updates to licensing provisions for successful deployment and regulation of digital wallets, within electronic payment regulations, and through developing banks (public and private) delivery systems of banking accountability via digital transformation.

Significant Fintech Solutions That Are Dramatically Changing the Banking Sector in Nepal

Fintech is dramatically changing the banking sector in Nepal in various ways. Fintech solutions that are significant today include:

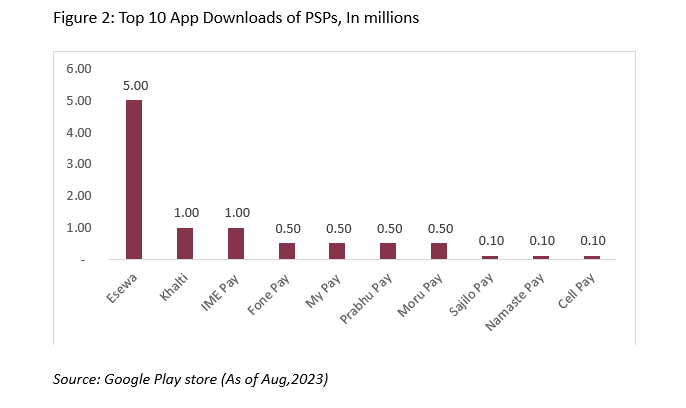

1. Digital Payments and Wallets:

Digital payment platforms and mobile wallets including eSewa, Khalti, and IME Pay are ubiquitous in Nepal today. While

2. Peer-to-peer Lending and Crowdfinding:

Peer-to-peer lending (P2P) platforms have emerged as an alternative to loans through traditional banks the past couple of years for individuals. It has been impactful to small-businesses and start-ups in Nepal that have difficulty obtaining loans through banks due to the collateral needed to obtain a traditional loan in the past. Similarly, there has been uptake in crowdfunding platforms that allow entrepreneurs to fund innovative projects or social causes (crowdfunding is similar to community and individual philanthropy) where people or individuals pull their money together for purposes other than sharing ownership in a company or receiving rewards for taking the risk or donating. Crowdfunding platforms represent an additional funding mechanism for innovations such as a certain community solving a problem together, supporting charities, or boosting an innovative idea into implementation.

3. Blockchain and Cryptocurrencies

In Nepal, blockchain is in its infancy but has strong potential to disrupt the banking and financial services sector. Blockchain offers a safer and more transparent mechanism for recording transactions and mitigating fraud, thereby enhancing confidence in the financial system. While a few banks have begun to investigate using blockchain technology for cross-border payments, which might markedly reduce transaction processing time and costs, the importance of the technology in the future cannot be overstated.

In contrast, cryptocurrencies remain a controversial topic in Nepal. To date, there is no formal restriction to using cryptocurrencies, and the growing and dynamic NFT and digital currencies in the world has triggered discussions on how cryptocurrencies will fit into the financial system in Nepal.

4. Regtech and Suptech

Regulatory technology (regtech) and supervisory technology (suptech) are referred to as fintech-related solutions used to enable and streamline financial compliance regulation and regulatory oversight, respectively. In Nepal, regtech solutions will enable banks to begin automating compliance and reporting, reducing manual burden and enhancing data reporting in compliance with regulatory requirements. This is especially pertinent in Nepal, as the NRB (Nepal Rastra Bank) will continue to set new regulations keeping pace with the burgeoning fintech space. In addition, suptech is a regulatory technology that can be used by a regulator in Nepal, such as the NRB, to monitor and oversee institutions and their exposure to risk at the same time. This gives us much more confidence in the stability and soundness of the financial system in Nepal.

Opportunities for Fintech in Nepal

Fintech presents several opportunities for Nepal’s banking sector. The most significant ones include:

1. Financial Inclusion

One of the primary objectives of fintech in Nepal is to facilitate financial inclusivity. A significant portion of Nepal’s populace, particularly those residing in rural areas, are either unbanked or underbanked. Fintech solutions give the opportunity to provide financial services to historically unattended persons. This has the potential to close the financial café between urban banks and rural banks and eradicate poverty by giving individuals access to savings, credit, insurance, and investment opportunities.

2. Increased Efficiency

Fintech can facilitate greater efficiency and economy to proceed with banking operations. Lending approvals, customer on boarding, and conduct compliance check can save banks operational costs and provide faster services to customers by automating the process. Additionally, customer satisfaction can potentially rise with the growing demand for banking with speed and at convenience.

3. Greater Safety

Increased cyber threats make it imperative to provide security over financial transactions. Fintech utilizes advanced technologies, such as artificial intelligence (AI), machine learning (ML), and blockchain, to enhance security over financial transactions and to reduce fraud protection. Employing these technologies will help banks earn trust with their customers and secure sensitive financial data.

4. Innovative products and services

Fintech promotes innovation and allows banks to introduce innovative products and services to satisfy customers through customization. For example, digital banks or neo banks provide a fully online banking process without a physical footprint. In another example, robo-advisors provide investment advisory services at a lower cost than traditional financial advisors while still providing customization.

Obstacles to Fintech in Nepal

While opportunities abound, there are challenges to using fintech in Nepal. The challenges include:

1. Regulatory Hurdles

The NRB has made some impact toward overseeing fintech, but there is still significant need for more detail and clarity in overseeing new technologies such as blockchain, cryptocurrencies, and AI. Vague regulations often limit innovation and create uncertainty for fintech startups seeking to enter the market.

2. Barriers to Digital Literacy

While rates of internet and smartphone use are high and increasing, digital literacy may still act as significant barriers to using fintech in Nepal. Many Nepalese people - and especially those living in rural areas - are unfamiliar with digital financial services and may be reticent to adopt them. Financial institutions and fintech companies should invest in public education to inform citizens about the risks and benefits of using fintech in Nepal.

3. Infrastructure Limitations

While advancements have been made in banking and telecommunications infrastructure in Nepal, it is still evolving and cannot fully support fintech solutions at scale. For example, banks that are dependent on mobile banking to reach users in more remote areas of Nepal may be limited by the poor and unreliable internet connectivity. Thus, high quality, reliable and persistent digital infrastructure is required in Nepal to support growth of fintech.

4. Cybersecurity Threat

With the increased adoption of fintech comes increased risk related to cyberattacks. Cybersecurity should be a priority in all currently operating financial institutions in Nepal with an emphasis on increased investment into cybersecurity technologies aimed at hacking, fraud, and data breaches. All who seek to transform growing adoption of fintech in Nepal should assist in building a strong cybersecurity foundation for current and future trust in digital financial services.

The Future of Fintech in Nepal

The future of fintech in Nepal seems to hold great promise towards revolutionizing the banking sector as well as enhancing financial inclusion. As there's more of integration of fintech, by extension, the financial system will benefit from innovation, efficiency, and transparency. Nonetheless, to optimize the opportunities of fintech, difficulties in terms of regulation, infrastructure, and digital inclusion need to be tackled in Nepal.

Nepal can bite the baguette of fintech fully if efforts are made in the direction of fair regulatory regimes, developing digital infrastructure and the strides taken to enhance education specifically information and communication technology. This will facilitate a new way of banking in Nepal as it will be the collective efforts of the banks, fintech companies, regulators and the government. Fintech only does not come as a hype. Wholeness is brought into the system that was never felt before through the provision of financial services. The advent of this digital world may stamp a wider leverage of fintech in future banking systems in Nepal, agriculture financing will also be within reach and the whole economy strengthened.